April 11, 2022

How can the life insurance industry improve its speed of offering to customers with more complex health issues?

Blog by Simon Jacobs, Director of Business Development, UnderwriteMe

The buying process for Protection products must, at times, leave consumers baffled. In a world where purchasing products of all kinds, including insurance, is immediate we still leave a percentage of our customers waiting for a decision and a price. At times customers and advisers will feel a lack of transparency over the next steps, timescales, and outcomes.

There haven’t been many revolutions in underwriting, things have improved steadily over the decades. Underwriting engines changed things by giving customers decisions at the point of sale, electronic GPRs are winning over an increasing number of doctors and, at UnderwriteMe, the Protection Platform helps manage expectations while giving advisers and consumers a choice of fully underwritten outcomes form a wide selection of insurers.

As an industry we need to accelerate to remain relevant to consumers of today and the future. Around a quarter of all customers end up in “manual underwriting” and this is where technology can help. The technology is available now.

It’s not only customers who will benefit, we can take some strain away from hard-pressed underwriting departments and reduce some of our reliance on health care professionals.

As the pandemic continues to have an impact on our lives, concern remains about the effect on health services. Waiting lists are increasing as seen on the NHS backlog data analysis, provided by the BMA in January 2022, showing over 6 million patients waiting for treatment, up from 4.4 million prior to the pandemic. One of the key drivers around this is that people are not presenting to their GP with their initial symptoms as they are unable to obtain an appointment time. Additionally, face to face appointments have reduced in number, staff vacancies are compounded by medical professionals having to isolate in line with Government guidelines.

Square Health, when looking at their virtual GP services, have seen dramatic increases – February 2022 saw a 46% increase in GP consultations when compared to the corresponding period in 2021 they saw a similar increase to Feb 2020, just before lockdown. Consultations are available 24 hours a day and individuals are using the service around the clock. There are an increasing number of repeat users, suggesting that once they have used the service once, customers are comfortable with an online experience compared with struggling to obtain an NHS appointment.

All of this has a knock-on effect for the Protection industry which relies heavily on medical information. It’s not hard to see how customers could face delays in getting the valuable Protection cover they need, especially if their application gets stuck in an underwriting work queue. UnderwriteMe data shows that, where cases are referred for medical evidence, 25% will go on risk if the evidence is received back within two weeks, that drops to just 5% when customers must wait for more than four weeks. Fortunately, technology is offering us a solution.

The key is ensuring advisers and customers feel informed and engaged with the Protection buying process and only the most complex of medical histories is seen by an underwriter. As an industry we’ve championed providing access to insurance to as many customers as possible. Spending more time assessing customers with challenging medical histories, giving them the individual attention and time, they deserve, can only be a good thing. We could argue that its these very customers who are in most need of the peace of mind of protection. The industry needs to continue to strive to service these customers as quickly as possible.

Pre-application tools and indicative decisions are helping advisers manage customer expectations and reduce waste as likely outcomes are clear and understood from day one.

Medical examinations are an important underwriting tool but also an unavoidable imposition for customers. The least we can do is process their information quickly and in the early part of 2022 we’ll automate both the requesting and underwriting of nurse screenings and blood tests. For customers we will strip days out of the process – no waiting for the request to get to the medical examination provider and no waiting for the underwriter to review the results. For insurers there are gains as the need to manually request a screening will be removed and underwriters will be deployed to focus on challenging underwriting rather than relatively straightforward work.

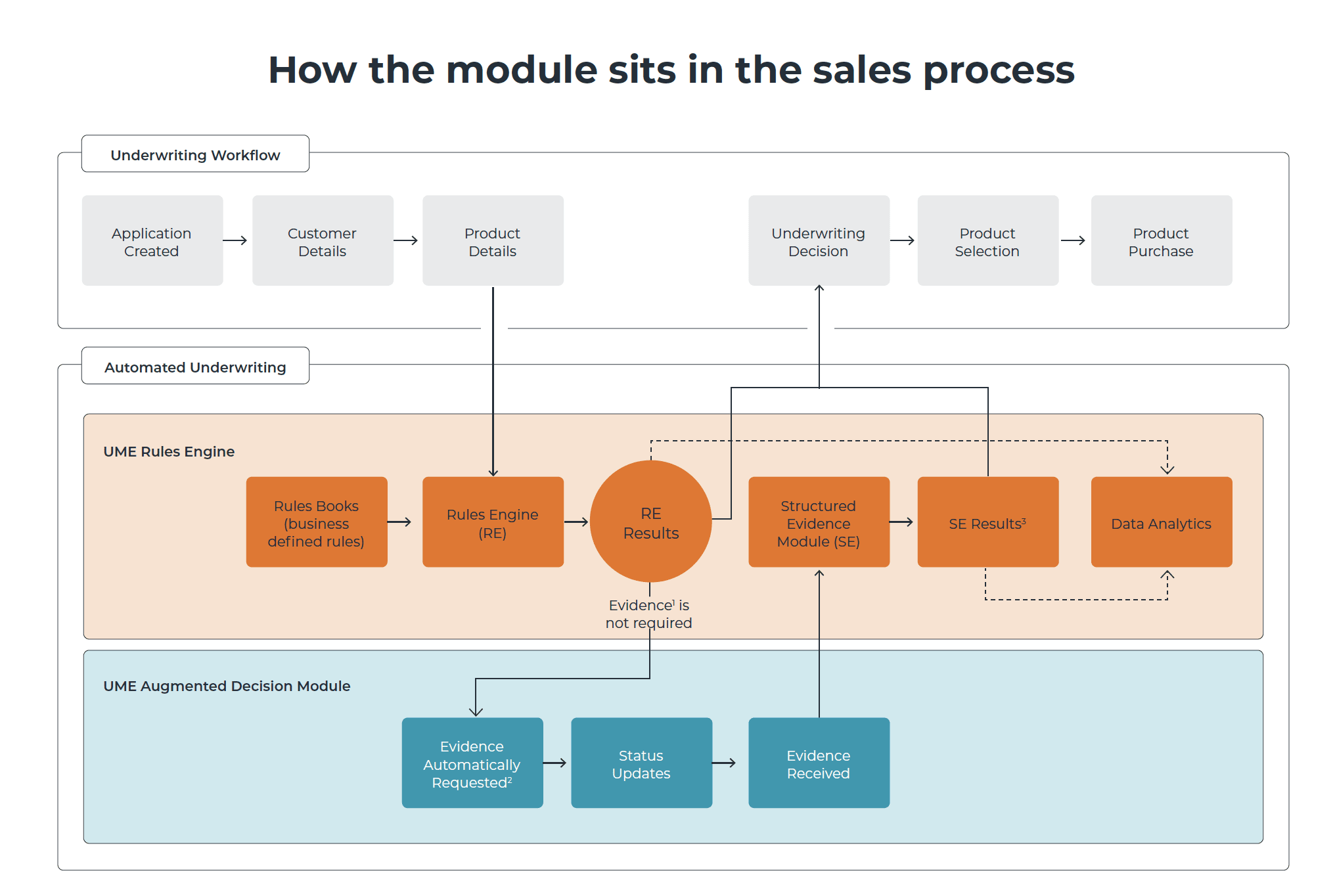

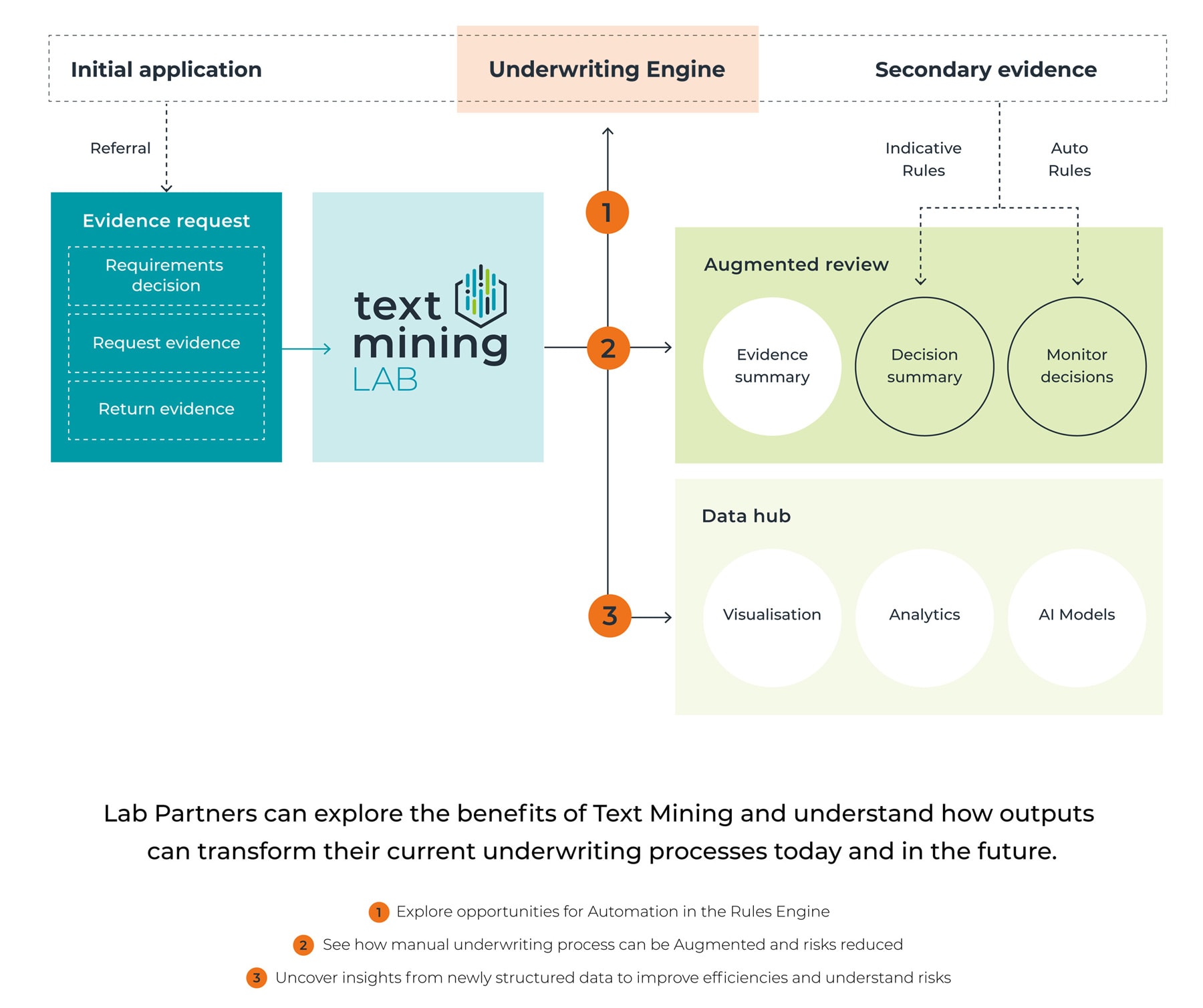

The biggest area of underwriting evidence is, as ever, reports obtained from doctors. Automating the assessment of this information has always seemed futuristic… but progress is rapid. Text Mining is allowing medical information to be condensed and turned into structured reports. Key risks are highlighted, information is chronological, repetition is removed, and “white noise” is stripped out. The advantages for underwriting departments are in reducing the time it takes to pour over pages of detailed information, reducing the risk of missing a key factor and allowing the underwriter to focus on what’s relevant. As we continue to learn with partner insurers, it will be possible to automate underwriting outcomes.

Further benefits will come for insurers as the data sitting behind this technology will grow, allowing them to better understand the value of medical evidence – reducing it where it adds little or no value and pointing the underwriting effort in directions that are truly useful.

All these initiatives will drive a slicker, quicker, more transparent journey, building customer and adviser confidence in Protection products. 2022 will see some big steps forward in the world of underwriting.