September 19, 2023

The Future of Underwriting – Carriers Aim to Meet Consumer’s Expectations with Automation

The Future of Underwriting – Carriers Aim to Meet Consumer’s Expectations with Automation

According to the 2023 Insurance Barometer Study, published by LIMRA, 41% of all US adults have an insurance need gap. This equates to 101 million adults and their families who are at risk should an unexpected illness or accident occur. How can the industry make a dent in this unmet need?

The first step is recognizing that consumer needs and expectations are changing, starting with the fact that younger generations have been conditioned to expect on-demand buying experiences. When they want products, they want them now. This same generation is beginning to start families, buy cars, buy homes, etc., which is leading to an uptick in insurance policy purchases.

Carriers are testing innovative ways to create experiences that address their customer’s expectations. Through this process, two trends have emerged 1) creating a personalized digital experience, and 2) adding underwriting automation to issue policies faster. In fact, offering accelerated underwriting and instant decisioning should be considered table stakes by now. With this backdrop in mind, how should carriers be thinking about transforming and/or improving their digital customer experiences?

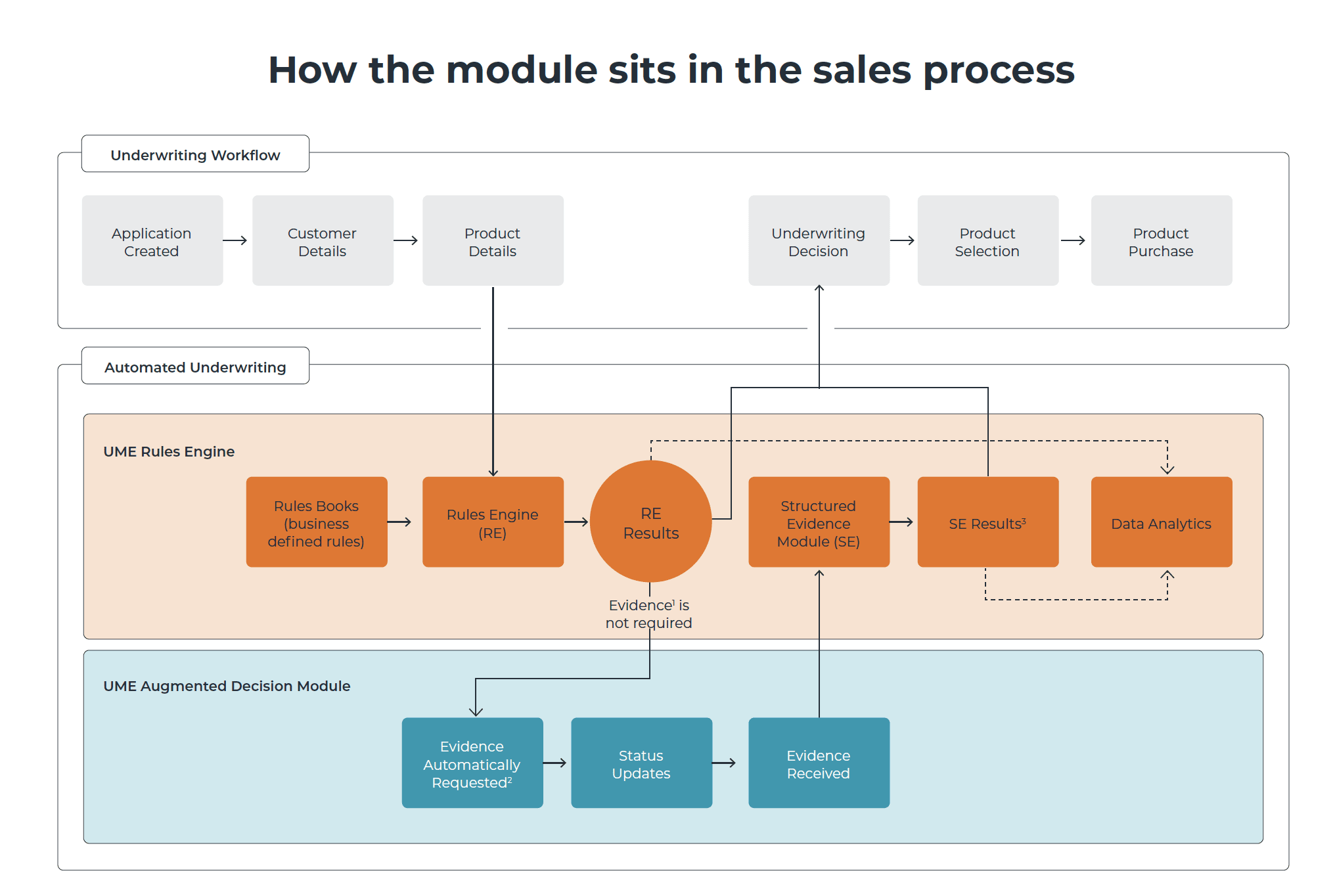

It starts with having the right platform. Moving away from legacy systems to allow for new tools and solutions is critical to surviving in a digital future. This allows carriers to take advantage of a new ecosystem of machine learning models, underwriting rules, and real-time predictive data sets that can be leveraged to make quality risk decisions while facilitating a streamlined digital underwriting experience. This remains the number one focus for carriers today.

Consumers and underwriters are at the center of it all

What does this mean for the future of underwriting as it relates to underwriters and consumers? For underwriters, recognizing that their unique skill set is required for the future is vital for retaining their talent, and enabling them to underwrite more effectively and efficiently is the key to providing the best outcomes for both carriers and customers. Complex underwriting does not go away; rather, ever-improving rules, new solutions, and new datasets will support the underwriter as they assess applicants.

The industry is continuously evolving in terms of new risks, ways to identify unknown risks, and understanding updated treatment options and corresponding prescriptions. Underwriters play a significant role in collaborating with other subject matter experts, i.e., data scientists and actuaries, to understand what this means for their respective decision-making processes.

Underwriters are central to the insurance ecosystem by helping to develop a positive bridge to the consumer while adequately assessing their risk. As carriers continue to keep consumer interests at the center of everything they do, underwriters hold the key to providing the best client journey possible. They are central to explaining decisions and providing clarity to the consumer as efficiently as possible while developing a seamless, noninvasive experience that keeps mortality/morbidity costs in check.

What does this mean for consumers? Quicker policy issuance, more personalized policies, and better digital buying experiences. Simple as that.

Evaluating Risk During Digital Underwriting

In today’s digital-first, data-driven underwriting environment, carriers continue to ask themselves, “How can we accelerate more users and provide a seamless customer experience while improving mortality and reducing risk?” The answer lies in understanding the intent of the end user.

Today, carriers largely provide a static user experience with strict underwriting rules and reflexive questions that depend on the responses an applicant fills in. Where they’re going, however, is toward a dynamic experience that adapts to the individual applicant’s intent and risk profile based on their digital behavior.

How an applicant navigates a digital application is incredibly telling of their truthfulness and intent. New solutions are available to help carriers better understand applicant intent and identify instances of nondisclosure during the application process.

While there are many things carriers are doing to get ready for the Future of Underwriting, here’s our take on four things you can do today:

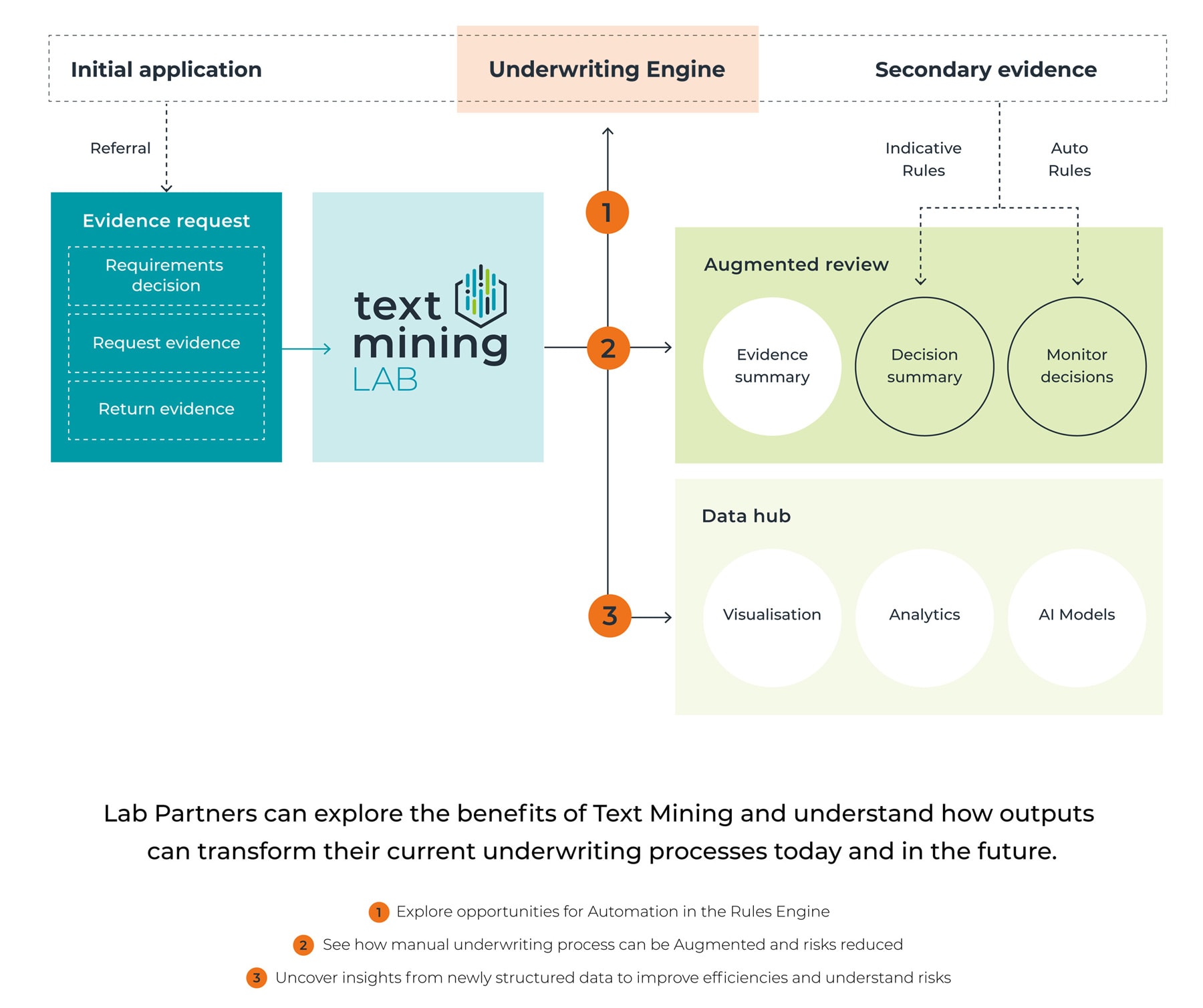

- Take advantage of an ecosystem of rules and models – with the right data sources – that doesn’t trade off mortality and morbidity and still offers an amazing customer experience. Learn more here.

- Enrich the role of the underwriter by optimizing the traditional underwriting process with the effective use of risk automation tools.

- Leverage behavioral data to predict applicant purchase intent.

-

- Create a better digital experience by predicting the purchase intent and channel preference of your applicants, allowing for more personalized experiences tailored to the individual applicant and more productive agent outreach and remarketing efforts.

- Protect your downside

-

- Identify and reduce Nondisclosure and Material Misrepresentation in real-time to triage applicants at the point of quote and drive the appropriate next-best action. To make real-time underwriting decisions with confidence, carriers need to lean on solutions that identify risks that were previously undiscoverable. Learn more about real-time Nondisclosure Solutions here.

Visit us at UnderwriteMe and ForMotiv to learn more about how we can help.

Or Connect with Scott Hunt, AVP, UnderwriteMe, and Woody Klemmer, Head of Growth at ForMotiv