October 27, 2021

TMA on the Mortgage Protection market

With the Pandemic easing and businesses returning to some sort of normality, how has the Mortgage market changed?

In my view the market has not changed dramatically, but there are definitely learnings, that we should take forward into our businesses, to make them more efficient, more cost effective and better equiped to shape and future-proof all of our businesses.

The Reflect, Refuel and Refire mentality was one of the key drivers for all business owners at the start of the pandemic.

We have seen some positive changes in how businesses operate, in terms of more flexible working for employees, and some greater use of technology, which has translated into how they engage with their customers, offering a more flexible service, and choice lead approach to engaging and fulfilling the needs of their customers.

We have clearly seen some personal changes to customers circumstances, both positive and regrettably negative for others. Perhaps for many COVID provided a reflection or reprioritisation on what is personally important in life, in terms of Health, Wellbeing, Relationships, Family and Mental Health?.

My view is that this affords opportunity for intermediaries to engage with their customers to help overcome their fears, support their financial ambitions, and educate with financial solutions, all with a view to dilute the risks through true financial planning and advice.

There are still some key fundamentals that will continue to challenge the UK housing Market, such as the lack of available housing stock, Renters to Homeowners support, and the quality of some rental properties.

Equally, increasing property values, impacts deposit saving for First Time Buyers, and customer affordability in high property price areas.

In addition post pandemic there has been an increasing focus by the regulator in some large topic areas, which albeit are welcome to protect both consumers and our industry, however challenging in terms of freeing up ‘customer time’ to interpretate, reflect, and consider business impacts within some smaller to medium sized businesses.

What is TMA’s view of the Mortgage market for 2022 – What are the risks and opportunities for brokers?

At this stage, there is still much debate about the outlook for 2022.

What I can say with confidence, is it always seems impossible until its done! (Nelson Mandela):

My top tips for brokers would be:

- Plan Early for 2022.

- There are still huge opportunities to support customers needing financial advice.

- Segment your customer contact strategy.

- There are endless opportunities to educate consumers, to financially protect themselves, their familes and partners, and their lifestyle too!.

- Customer retention and regular engagement should be at the heart of every intermediary business.

- The Re-Mortgage and Product transfer market will remain buoyant, review protection needs.

- Building long term recurring revenue, as opposed transactional revenue remains hugely important.

- Keep you customers and business safe, don’t suffer in silence – seek support!

- Don’t return to pre-pandemic practices, take the learning with you!

We’ve had 18 months of working under the Pandemic – how has that affected the way you work with Lenders?

I believe interaction with our lenders has remained strong, and again we have utilised telephony and technology to bridge the gap of loosing face to face meetings.

I believe it has made us all think more clearly about what time we afford to our meetings, and the value and objectives we need to gain from our conversations. It has in essence provided another median for communication.

When facilitating the support to our intermediaries from lenders we conducted training, market updates, and various other messaging via zoom.

Lenders have equally been looking at how they engage with intermediaries, again offering a wider range of technology solutions, in addition to pre-pandemic support mechanisms.

Are you able to talk about any future developments at TMA that will help mortgage brokers?

I have touched on two areas above, which are Regulatory support and use of technology, both which are key drivers for TMA in supporting our intermediaries. Without giving away the crown jewels, we will continue to do the things we do very well in supporting our members. Our LSL financial services footprint in the financial services sector is very strong, and we have publicly stated that we have ambitious plans to grow the support to the Financial Services sector. Stay or become connected to TMA, is all I can say!

What do you think the key is to Mortgage Protection?

It’s vitally important to make sure the client understands the need for protecting themselves and their families/partners right from the first conversation. We all know clients come to advisers to facilitate the purchase of their dream home, or support other financial transactions. It is our job as intermediaires to ensure they understand the importance of protecting the debt, lifestyle and loved ones. Simple real-life terminology brings the focus on protection to life!. Gaining the clients commitment right from the start of the conversation is key, to ensure the budget and affordability encompasses protection.

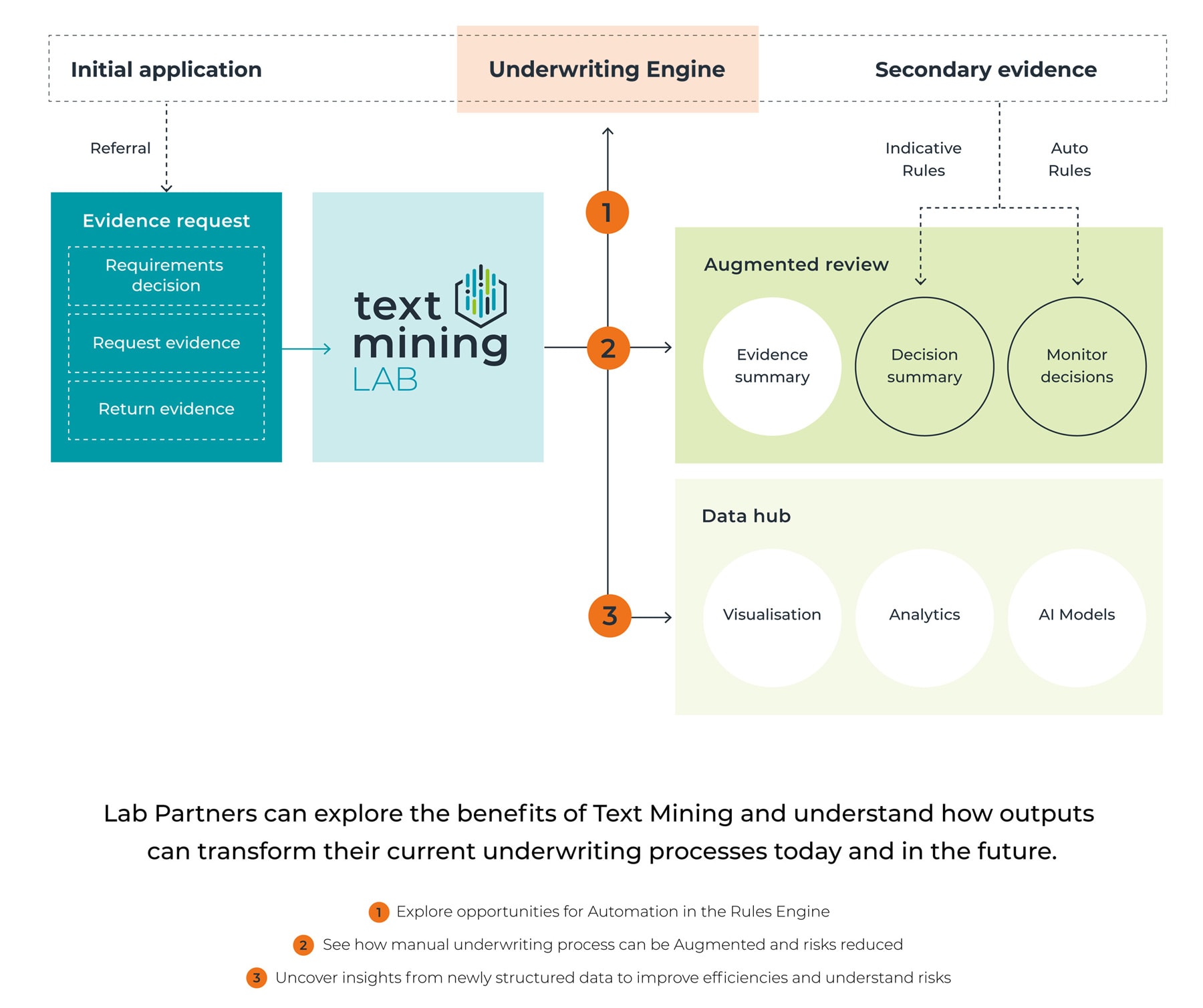

You joined the Protection Platform what was the driver for joining and how has that worked for TMA? How do you think the Protection Platform can help advisers in writing Protection when related to mortgage business?

At TMA we are always looking for new services and technology to help advisers do the best job for their clients. When we identified with how the Underwriteme platform could save advisers time for those clients where they would otherwise have to do a huge amount of additional research, we thought this was a great solution. For those clients who have a pre-existing medical condition or family history it can navigate and reduce the manual process considerably. With the ability to submit multiple applications to different providers with one input, again for those on the platform it potentially supports the efficiency for intermediaries.

What’s your message for TMA colleagues and fellow mortgage distributors for the rest of the year?

To Distributors: We must all ensure we absolutely ‘fly the flag’ for consumer advice.

The bad news is time flies, but the good news is you’re the pilot!

For colleagues: Lets secure the foundations ready to articulate our plans for 2022 to hit the ground running.